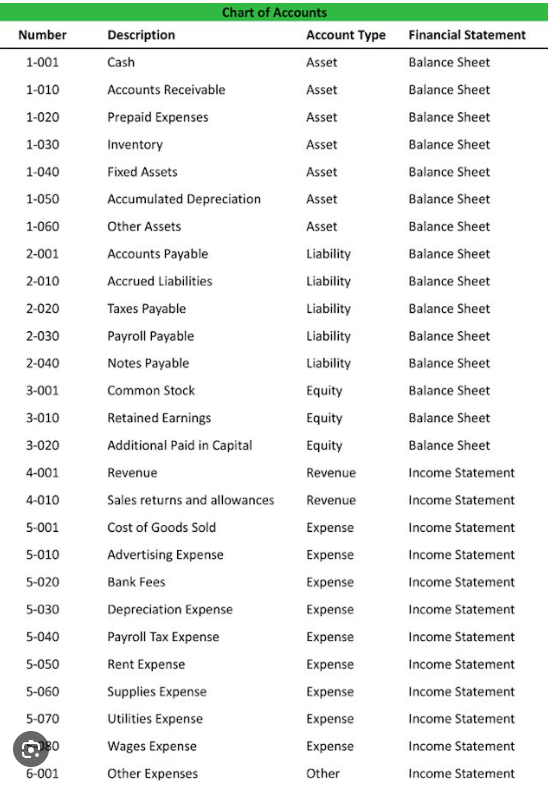

This chart of accounts is suitable for use with GAAP.

Since the oft advised approach to COA design is sub-optimal, this page uses a more robust approach.

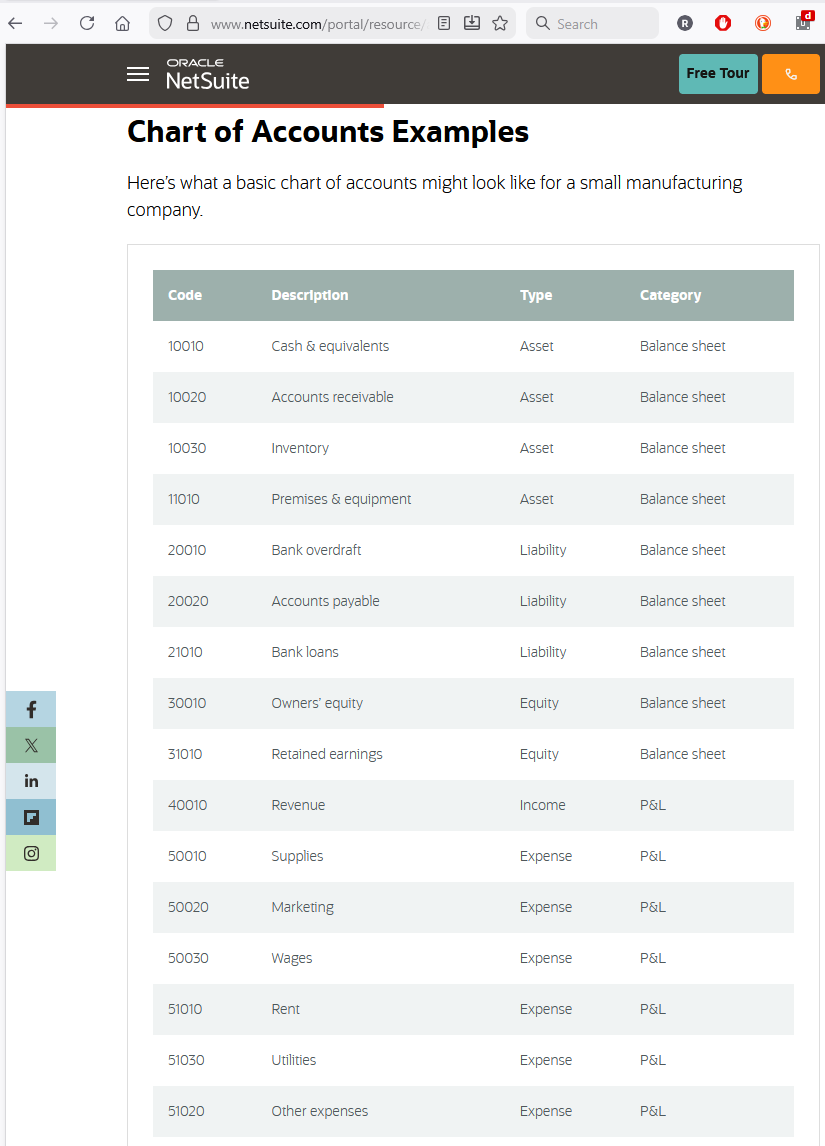

For example, one renowned accounting software producer introduces their COA this way.

A promising start.

The detail put into a COA does set the ceiling for financial analysis. If the COA does not capture a data point, it will not make it to a financial report. A well-structured COA will support accurate, compliant financial statements and misclassified accounts can distort key metrics, trigger audits and make correctly applying complex guidance, especially guidance promulgated by the IASB or FASB, practically impossible.

But, when it pivots to the challenges, it becomes self-contradictory.

The page correctly points out that “a well‑structured COA supports accurate, compliant reporting.” But then points to overcomplication suggesting that "A chart of accounts can become unnecessarily complex if it contains too many categories and subcategories."

However, an oversimplified COA does not make details go away. It simply moves them off the COA, which is precisely where inconsistencies, misclassification occur and remain hidden until discovered by an auditor or, with more dire consequences, regulator.

Then comes the second contradiction.

The oversimplification mantra does nothing to address "Inconsistent naming and coding [that] can cause staff to interpret accounts in different, unintended ways."

Quite the opposite. It encourages, perhaps even forces, junior accounting staff, the staff least qualified to make the recognition and measurement to make recognition and measurement decisions.

Finally, it drops these pearls of wisdom.

While a provider of cloud-based accounting software can be forgiven for implying that only cloud-based accounting software will facilitate dimensionality, why would it encourage the use of ad hoc subledgers to plug holes in a poorly designed COA when it does nothing to address one of the challenges it discussed earlier?

Why would renowned accounting software producer provide such substandard advice?

Perhaps, as a producer of accounting software, it bears no responsibility for how that software is employed and selling a seemingly simple and carefree solution to a complex and intractable problem helps sell more software. Or, perhaps, we are just being cynical.

In any event, fortunately, accountants have judgment which they are free to use in any way they deem reasonable.

So while accounting software producers are free to suggest using such a primitive account structure while allowing staff to add willy nilly, ad hoc accounts, the chief accountant is free to just say no.

Specifically, the systemic risk that software vendors often choose to ignore: if the COA does not have a slot for a non-negotiable accounting rule, that rule has to be managed manually. From an AI/Data perspective, manual workarounds are dirty data. From an accounting perspective, they are internal control deficiencies. Deficiencies that in a high stakes environment such as SOX compliance can lead to very serious consequences.

Sarbanes–Oxley (edited, link):

Sec. 1350. Failure of corporate officers to certify financial reports

(a) CERTIFICATION OF PERIODIC FINANCIAL REPORTS- Each periodic report containing financial statements filed by an issuer with the Securities Exchange Commission pursuant to section 13(a) or 15(d) of the Securities Exchange Act of 1934 (15 U.S.C. 78m(a) or 78o(d)) shall be accompanied by a written statement by the chief executive officer and chief financial officer (or equivalent thereof) of the issuer.

(b) CONTENT- The statement required under subsection (a) shall certify that the periodic report containing the financial statements fully complies with the requirements of section 13(a) or 15(d) of the Securities Exchange Act of 1934 (15 U.S.C. 78m or 78o(d)) and that information contained in the periodic report fairly presents, in all material respects, the financial condition and results of operations of the issuer.

(c) CRIMINAL PENALTIES- Whoever--

(1) certifies any statement as set forth in subsections (a) and (b) of this section knowing that the periodic report accompanying the statement does not comport with all the requirements set forth in this section shall be fined not more than $1,000,000 or imprisoned not more than 10 years, or both; or

(2) willfully certifies any statement as set forth in subsections (a) and (b) of this section knowing that the periodic report accompanying the statement does not comport with all the requirements set forth in this section shall be fined not more than $5,000,000, or imprisoned not more than 20 years, or both.'.

Furthermore, the SEC (link) now has the power to claw back executive bonuses even if the executive didn't personally commit fraud.

Prosecutors may also stack SOX violations with Section 1519 (Falsification of Records) or updated Wire and Mail Fraud statutes (18 U.S.C. §§ 1341, 1343), which carry their own 20-year maximums.

Ouch.

The Simplicity trap: why "lean" charts of account are an internal control failure

Modern ERP implementation guidance frequently advocates for a "simplified" or "lean" COA. The argument is that fewer accounts reduce complexity and user error. We argue the opposite: oversimplification in the G/L does not eliminate complexity. It merely decentralizes it. By removing the granular "forced-choice" mechanism of a well-designed COA, organizations inadvertently delegate high-level technical accounting decisions to junior staff, increasing the risk of misclassification, reconciliation failure and audit non-compliance.

- The fallacy of the "clean" ledger

The push for a lean COA is often driven by a desire for aesthetic "cleanliness" in financial reporting. However, accounting requirements (IFRS, US GAAP, and Local Statutory) remain inherently complex. When a COA is stripped of specific categories, the data does not vanish. Instead, it migrates:

- Unstructured sub-ledgers: where data governance is weak and compliance overlooked.

- Manual spreadsheets: the shadow ledgers that haunt year-end reconciliations.

- Ambiguous dimensions: where proper classification is ignored to facilitate high-volume data entry.

- The COA as control mechanism

A granular COA is more than a list of accounts. It is a preventative control.- Forced technical decisions: if a junior accountant is presented with 40 possible classifications related to employee benefits, they will make absolutely certain they pick the correct one particularly if they know that if the "Other employee related accruals" balance exceeds 1% of all employee benefits, serious questions will be asked.

- The escalation trigger: if a junior accountant is presented with 40 possible classifications related to employee benefits, they will make absolutely certain they check before classifying a particular item incorrectly. If they are not certain, they will ask. That is normal. That is how junior staff become senior staff. Note: if they ask the same question twice, it is a good indication that junior staff should, without delay, become former junior staff. This is how compliance is actually achieved.

- The Multi-jurisdictional issues

For global entities, simplification is an executive luxury that creates a subsidiary nightmare. Local statutory requirements (such as the French Plan Comptable) demand an approach that is different from the IFRS report submitted to stakeholders in London or a US GAAP report for the minority shareholders who acquired their stake on the New York Stock Exchange. At some point, local teams must know when a G/L item can be plugged into a reporting package, when it must be adjusted before being plugged in and, most importantly, when it cannot be adjusted at all, but must be completely re-recognized and remeasured. Unambiguous accounts with unambiguous titles (and XBRL tags) go a long way to making these distinctions clear - Dimensions and determinants

Some dimensions (e.g. FVOCI or FVNI, the currency in which monetary assets are denominated, accumulated depreciation or amortization or depletion or even impairment, the function of an expense, etc.) are crucial for IFRS | GAAP compliance and should be hard wired. Other dimensions (department, customer type, geographic region, etc.) are nice to have, but will not cause an audit report to become qualified. Having a COA clearly shows each new hire where that line is simply makes both compliance and operations management simpler.

Instead of the traditional approach to account identification, a hierarchical, delimited scheme is used.

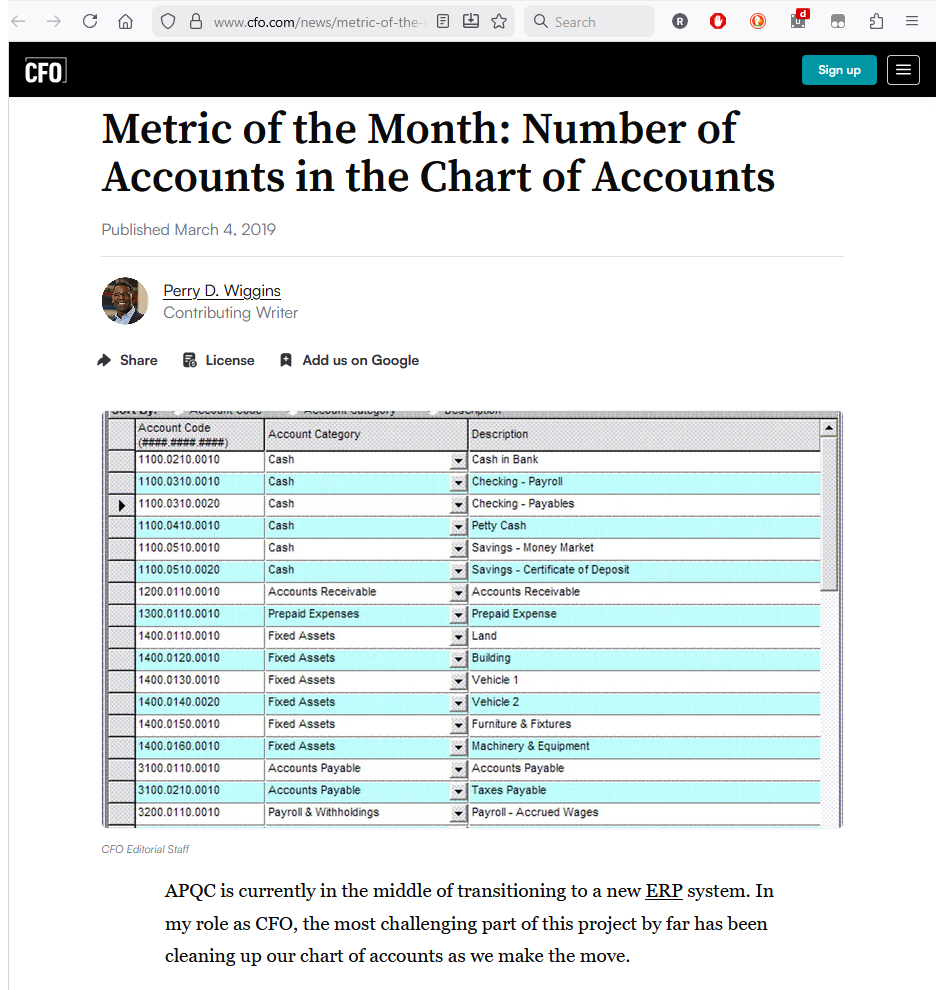

For example, Googling "chart of accounts" brings up results such as these:

Most strictly adhere to the same, flat block structure that should have disappeared along with green eyeshades but, for some inexplicable reason, continues to hang on. Probably just sheer force of will or (as with the last two examples) legislative mandate.

The COA from Investopedia does take a baby step towards modernity by introducing one delimitation. But then it gets frightened by all that innovation and scurries back to the way it has always been done ¯\_(ツ)_/¯

However, adopting a flexible, expandable approach and then using it unwisely is likely to be much worse.

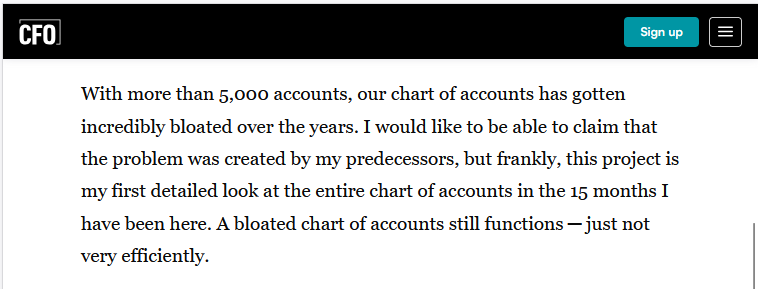

In this article (link / archive), the author makes some good points but, unfortunately, misses the big picture.

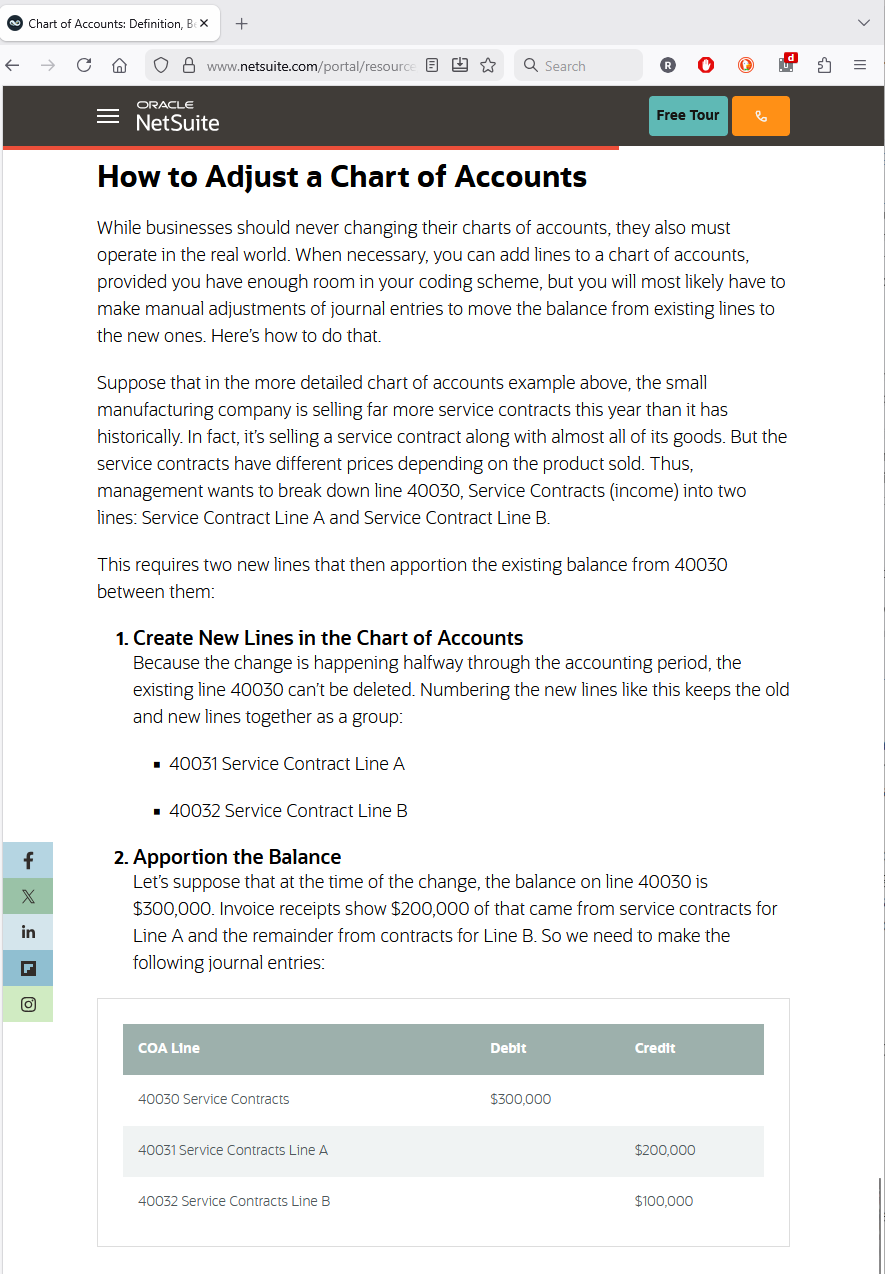

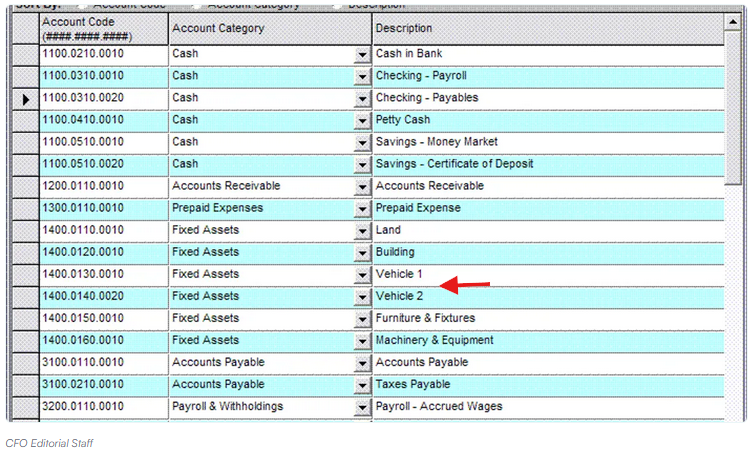

For example, 5,000 accounts does seem like bloat , but only if accounts are created for the wrong reason. While the snippet does not allow a drill down so may just be a case or careless labeling, adding individual fixed assets to a COA will certainly cause bloat. This information does not belong on a COA or in even a G/L. It belongs in a dedicated subledger comprising, for example all light-duty trucks (as opposed to heavy duty-trucks which, as a rule, have different lives).

Fortunately, the author then goes on to clearly identify the real culprit.

Without any doubt, allowing just any manager to add an ad hoc account unsystematically without any planning or forethought is certain to guarantee of a bloated, unworkable COA. A COA best deleted before it leads to consequences (such as a qualified audit report, or regulatory enforcement action, or, in a SOX reporting environment, something potentially much more severe).

Specifically, it is a Chief accountant's job to ensure proper controls over the company’s fundamental accounting structure. While this may seem like recipe for centralized inflexible accounting, allowing managers to add accounts willy-nilly, particularly managers at international subsidiaries whose working knowledge of local legislation and local enforcement is likely much more thorough than their knowledge of IFRS | US GAAP and the compliance demands of regulators such as the SEC, FSA, FCA, AMF or BaFin is worse.

A CFO’s job is to plan, budget, and forecast. More importantly, it is to maintain a working relationship with important creditors and represent the company to investors. Delegating the actual, day-to-day task of making certain the company's accounts not only provide managers with the information they need but facilitate IFRS | US GAAP compliant financial reports to professionals explicitly trained and experienced in these matters, is probably the more rational choice. In other words, CFOs are usually not particularly good accountants. Accountants are good accountants.

This also implies that taking professional advice from a site aimed at the former tends to not be as effective as taking it from one aimed at the latter.

Note: as the script on this page (link) illustrates, account numbering optional. The hierarchy itself dictates structure.

Vague COAs requiring ad hoc subledgers may even be dangerous.

A frequently repeated recommendation (discussed above) is to keep the chart of accounts as simple and high-level as possible, and to “push detail” into subledgers or dimensions when needed. In theory, this keeps the general ledger tidy. In practice, especially in international groups, it often produces the opposite of what good accounting requires: inconsistency, inaccuracy, and loss of control.

The problem is structural. If the COA is overly general and staff are allowed to create subledgers ad hoc, the system as a whole becomes fragmented. Each accountant, department, or subsidiary can develop its own unofficial structure under the same top-level accounts. Over time, what appears to be a single, consistent account in group reporting actually represents a patchwork of different local practices and interpretations.

This is particularly acute in cross-border groups. Consider a US parent that gives its foreign subsidiary a rudimentary US GAAP reporting package with a handful of broad lines to fill out. The subsidiary completes the package to keep the parent satisfied, even when the mapping from local GAAP to those broad US GAAP categories is approximate at best. If local staff are also free to “solve” gaps by building their own subledgers and coding schemes, the risk is that the reported numbers look acceptable on the surface, but are structurally wrong underneath.

The less familiar local staff are with IFRS or US GAAP, the greater this risk becomes. Giving them wide latitude to modify the underlying structure through subledgers and custom codes is effectively delegating COA design to the people least equipped to do it. The very issues many experts warn about—“inconsistent naming and coding” causing reconciliation problems, reporting gaps, and trouble rolling up results across departments or entities—are made worse, not better, by vague COAs plus ungoverned subledgers.

A detailed, well-designed chart of accounts is the opposite of unnecessary complexity. It is a control instrument. By defining accounts precisely and structuring them carefully, the entity reduces the scope for arbitrary local interpretation, makes mappings from local GAAP to IFRS | US GAAP repeatable and auditable, and limits the need for improvised substructures that nobody fully understands. In this context, “detail” is not a problem to be hidden in subledgers; it is the means by which the entity protects itself against quiet, systemic misclassification in its financial reporting.

The FASB (link) does not discuss the COA. To fill the void, we have been publishing a GAAP COA since 2010.

The FASB does not prescribe, define, or provide a standardized COA for organizations to follow. Instead, it focuses on high-level recognition, measurement and reporting principles and guidelines. Nevertheless:

- GAAP emphasizes how financial information is reported in financial statements, not the specific procedural steps, like account naming conventions, used in a company's internal bookkeeping.

- Organizations are free to create a chart of accounts tailored to their specific operational needs, provided the resulting financial reports comply with GAAP requirements.

- While they do not provide a list, the GAAP requires that the financial data captured by the chart of accounts adheres to principles like consistency, materiality and proper classification.

- A chart of accounts for a manufacturer will differ from one for a service provider. However each must reflect the same, basic accounting guidance.

The GAAP (or US GAAP, as it is known in the EU) COA was not our first.

In 2009, a client was not satisfied with the answer "the IASB does not publish a COA" saying "I don't care; I want one."

Many European Union member states have local legislation that prescribes a mandated chart of accounts. Practitioners accustomed to such accounting systems were looking for a similar, standard structure to use in an IFRS context. However, the IASB focuses on principles-based guidance and delegates the procedural aspects of accounting to practitioners, so has never included a COA in IFRS.

Companies must thus either design one themselves, or use an off-the-shelf version, such as posted here.

Since the client is always right, we created one.

Then, as recycling is good for the planet, we published a sanitized, generic version on this site. Within months, the IFRS COA became our most visited page.

After we published a GAAP COA, it became our most visited page.

Since most entities apply either IFRS or GAAP, our standardized COA has always brought up the rear, though Wikipedia does seem to like it.

The basic COA is suitable for a small business and freely available.

As a general rule, only publicly traded entities have a formal obligation to apply US GAAP guidance. As such, their accounting system must be robust enough to fulfill the extensive recognition and measurement guidance outlined in these standards.

Non-public entities in jurisdictions that do not mandate accounting practices have more flexibility and use any structure. Nevertheless, a sound account structure will help any business, regardless of size, optimize its operational efficiency and fuel data-driven decision-making regardless of size or ownership structure.

Since the ASC non-public entity guidance is the perfect backbone for accounting for all entities, COAs that reflect this guidance, such as those presented here, are useful to all but the smallest businesses.

These entities do not need to overthink their approach. They can simply use the default COAs supplied with small business solutions such as QuickBooks, Xero, or FreshBooks, which provide a simplified list of accounts that map directly to a Schedule C or Form 1120-S.

Provided they do the minimum to keep the IRS happy, no harm, no foul.

As anyone who has ever started a business knows, starting a business is the easy part. Keeping it running smoothly and profitably is where the real challenge lies. To help those just starting out, this site publishes workable, basic COAs, that can be expanded as needed, free of charge. After all, every business that survives the startup phase makes the business community richer and more diverse so is in everyone's best interest.

The expert COAs may be used by businesses of any size and also available in Excel format.

The advanced version is suitable for a single, large entity as well as a group of entities. The expanded version is a multi-dimensional COA designed for more complicated entities. The XBRL cross-referenced version is designed for publicly traded entities that face the task of drafting machine-readable financial reports required by some regulators.

A guide on how to set up the COA to serve various roles is presented on the implementation guidance page below.

Data can be loaded into an ERP in various ways (SQL, APIs, migration tools), but Excel remains the lingua franca of accounting, immediately understandable to virtually everyone. As illustrated on the implementation guide page (link), a COA may be flat or multidimensional, set up to handle multiple sub-ledgers or to include additional metadata.

To simplify the process of creating an ERP training file, Pro view includes a Python script that illustrates how to generate a dynamic hierarchical COA from the Excel source file, with posting and summation accounts defined automatically and, more importantly, flexibly. It also includes a script to map the output to a balance sheet and income statement (also in Excel).

Additional guidance on how to implement a COA is provided on this page.

Basic GAAP COA or go to Excel download page in Pro.

| Account Title | Account # | Depth | Balance | 1 |

| Assets | 1 | 0 | Dr | 2 |

| Cash, Cash Equivalents, and Short-term Investments | 1.1 | 1 | Dr | 3 |

| Cash and Cash Equivalents | 1.1.1 | 2 | Dr | 4 |

| Investments | 1.1.2 | 2 | Dr | 5 |

| Receivables and Contracts | 1.2 | 1 | Dr | 6 |

| Accounts, Notes and Loans Receivable | 1.2.1 | 2 | Dr | 7 |

| Contracts With Customers | 1.2.2 | 2 | Dr | 8 |

| Nontrade and Other Receivables | 1.2.3 | 2 | Dr | 9 |

| Inventory | 1.3 | 1 | Dr | 10 |

| Merchandise | 1.3.1 | 2 | Dr | 11 |

| Raw Material, Parts and Supplies | 1.3.2 | 2 | Dr | 12 |

| Work in Process | 1.3.3 | 2 | Dr | 13 |

| Finished Goods | 1.3.4 | 2 | Dr | 14 |

| Other Inventory | 1.3.5 | 2 | Dr | 15 |

| Accruals and Additional Assets | 1.4 | 1 | Dr | 16 |

| Prepaid Expense | 1.4.1 | 2 | Dr | 17 |

| Accrued Income | 1.4.2 | 2 | Dr | 18 |

| Additional Assets | 1.4.3 | 2 | Dr | 19 |

| Property, Plant and Equipment | 1.5 | 1 | Dr | 20 |

| Land and Land Improvements | 1.5.1 | 2 | Dr | 21 |

| Buildings, Structures and Improvements | 1.5.2 | 2 | Dr | 22 |

| Machinery and Equipment | 1.5.3 | 2 | Dr | 23 |

| Furniture and Fixtures | 1.5.4 | 2 | Dr | 24 |

| Right of Use Assets (Classified as PP&E) | 1.5.5 | 2 | Dr | 25 |

A right to use an asset is a contractual right. Thus, the right-to-use asset (ROU) is, strictly speaking, always intangible. Nevertheless, the FASB-defined XBRL taxonomy includes: PropertyPlantAndEquipmentAndFinanceLeaseRightOfUseAssetAfterAccumulatedDepreciationAndAmortizationAbstract.

This implies that the right to use, for example, a building would comprise PP&E.

Note: provided the right-of-use asset is recognised on the balance sheet, the guidance (ASC 842-20-45-1 to 3) is flexible about how it is presented. For example, a leased building may be presented within the “Buildings” line item rather than on a separate “right-of-use asset” line, as long as the notes explain that the amount relates to a leased (right-of-use) building rather than an owned building. From an internal accounting perspective, the building could thus be posted either to the Buildings account with a metadata flag indicating that it is an ROU or to the ROU account with metadata describing the underlying asset as a building.

| Additional Property, Plant and Equipment | 1.5.6 | 2 | Dr | 26 |

| Construction in Progress | 1.5.7 | 2 | Dr | 27 |

| Intangible Assets Excluding Goodwill | 1.6 | 1 | Dr | 28 |

| Intellectual Property | 1.6.1 | 2 | Dr | 29 |

| Computer Software | 1.6.2 | 2 | Dr | 30 |

| Trade and Distribution Assets | 1.6.3 | 2 | Dr | 31 |

| Contracts and Rights | 1.6.4 | 2 | Dr | 32 |

| Right of Use Assets | 1.6.5 | 2 | Dr | 33 |

A right to use an asset is a contractual right. Thus, the right-to-use asset (ROU) is, strictly speaking, always intangible. Nevertheless, the FASB-defined XBRL taxonomy includes : PropertyPlantAndEquipmentAndFinanceLeaseRightOfUseAssetAfterAccumulatedDepreciationAndAmortizationAbstract.

This implies the right to use, for example, a building should be classified an ROU within PP&E (above) even though the right is clearly intangible.

With intangible assets, such issues do not arise.

However, while both are clearly intangible, a, for example, leased patent differs from an owned patent. Nevertheless, recognizing both owned and leased patents on the same "Patents" account would not be incorrect, and would actually be preferable, provided additional metadata (facilitating the required footnoted discloses) is associated with the leased patents.

Alternatively, while not particularly elegant, separate "Patent" and "Right-to-use Patent" accounts could be used. While it would lead to fragmented and counterintuitive accounting, it would not be inconsistent with the the guidance.

ASC 842-20-45-1 states (emphasis added): A lessee shall either present in the statement of financial position or disclose in the notes all of the following: a. Finance lease right-of-use assets and operating lease right-of-use assets separately from each other and from other assets ...

ASC 842-20-45-2 clarifies this guidance by stating: If a lessee does not present finance lease and operating lease right-of-use assets and lease liabilities separately in the statement of financial position, the lessee shall disclose which line items in the statement of financial position include those right-of-use assets and lease liabilities.

In practice, the preferred approach would be to recognize, for example, both owned and leased patents as "Patents" and simply provide additional discourse of the values of the leased versus owned patents.

It would not, however, be incorrect to recognize owned patents as "Patents" and leased patents as "Rights to Use Patents" in which case, assuming the values are clearly distinguished on the balance sheet, they would not need to be reiterated in the footnotes.

| Crypto Assets | 1.6.6 | 2 | Dr | 34 |

While crypto assets have more in common with financial assets than intangible assets, ASC 350-60-15-1.a defines: a. Meet the definition of intangible assets as defined in the Codification ... d. Are secured through cryptography... The 2026 FASB-approved XBRL taxonomy (link) likewise places CryptoAssetFairValue on the balance sheet as a separate line item directly below intangible assets and above right-of-use assets.

| Additional Intangible Assets | 1.6.7 | 2 | Dr | 35 |

| Acquisition in Progress | 1.6.8 | 2 | Dr | 36 |

| Goodwill | 1.7 | 1 | Dr | 37 |

| Liabilities | 2 | 0 | (Cr) | 38 |

| Payables | 2.1 | 1 | (Cr) | 39 |

| Trade Payables | 2.1.1 | 2 | (Cr) | 40 |

| Interest Payable | 2.1.2 | 2 | (Cr) | 41 |

| Dividends Payable | 2.1.3 | 2 | (Cr) | 42 |

| Other Payables | 2.1.4 | 2 | (Cr) | 43 |

| Accruals, Deferrals and Additional Liabilities | 2.2 | 1 | (Cr) | 44 |

| Accrued Expenses | 2.2.1 | 2 | (Cr) | 45 |

| Deferred Revenue and Refund Liabilities | 2.2.2 | 2 | (Cr) | 46 |

| Taxes Other Than Payroll | 2.2.3 | 2 | (Cr) | 47 |

| Additional Liabilities | 2.2.4 | 2 | (Cr) | 48 |

| Financial Liabilities | 2.3 | 1 | (Cr) | 49 |

| Notes Payable | 2.3.1 | 2 | (Cr) | 50 |

| Loans Payable | 2.3.2 | 2 | (Cr) | 51 |

| Bonds | 2.3.3 | 2 | (Cr) | 52 |

| Other Debts and Liabilities | 2.3.4 | 2 | (Cr) | 53 |

| Lease Obligations | 2.3.5 | 2 | (Cr) | 54 |

| Derivative Liabilities | 2.3.6 | 2 | (Cr) | 55 |

| Commitments and Contingencies | 2.4 | 1 | (Cr) | 56 |

| Customer Related Contingencies | 2.4.1 | 2 | (Cr) | 57 |

| Litigation and Regulatory | 2.4.2 | 2 | (Cr) | 58 |

| Additional Obligations | 2.4.3 | 2 | (Cr) | 59 |

| Commitments | 2.4.4 | 2 | (Cr) | 60 |

| Equity | 3 | 0 | (Cr) | 61 |

| Equity, Attributable to Parent | 3.1 | 1 | (Cr) | 62 |

| Stockholders Equity at Par | 3.1.1 | 2 | (Cr) | 63 |

| Additional Paid-in Capital | 3.1.2 | 2 | (Cr) | 64 |

| Retained Earnings (Accumulated Deficit) | 3.2 | 1 | (Cr) | 65 |

| Appropriated | 3.2.1 | 2 | (Cr) | 66 |

| Unappropriated | 3.2.2 | 2 | (Cr) | 67 |

| Deficit | 3.2.3 | 2 | Dr | 68 |

| In Suspense | 3.2.4 | 2 | Zero | 69 |

| Accumulated Other Comprehensive Income | 3.3 | 1 | Dr or (Cr) | 70 |

| Other Equity Items | 3.4 | 1 | Dr or (Cr) | 71 |

| ESOP Related Items | 3.4.1 | 2 | (Cr) | 72 |

| Stock Receivables | 3.4.2 | 2 | Dr | 73 |

| Treasury Stock | 3.4.3 | 2 | Dr | 74 |

| Additional Equity Items | 3.4.4 | 2 | (Cr) | 75 |

| Owners Equity | 3.5 | 1 | (Cr) | 76 |

| Partner's Capital | 3.5.1 | 2 | (Cr) | 77 |

| Member's Equity | 3.5.2 | 2 | (Cr) | 78 |

| Non-share Equity | 3.5.3 | 2 | (Cr) | 79 |

| Non-controlling Minority Interest | 3.6 | 1 | (Cr) | 80 |

| Revenue | 4 | 0 | (Cr) | 81 |

| Recognized Point of Time | 4.1 | 1 | (Cr) | 82 |

| Goods | 4.1.1 | 2 | (Cr) | 83 |

| Services | 4.1.2 | 2 | (Cr) | 84 |

| Recognized Over Time | 4.2 | 1 | (Cr) | 85 |

| Products and Projects | 4.2.1 | 2 | (Cr) | 86 |

| Services | 4.2.2 | 2 | (Cr) | 87 |

| Adjustments | 4.3 | 1 | Dr | 88 |

| Variable Consideration | 4.3.1 | 2 | Dr | 89 |

| Consideration Paid Payable to Customers | 4.3.2 | 2 | Dr | 90 |

| Other Adjustments | 4.3.3 | 2 | Dr | 91 |

| Expenses | 5 | 0 | Dr | 92 |

| Expenses (Classified by Nature) | 5.1 | 1 | Dr | 93 |

| Material and Merchandise | 5.1.1 | 2 | Dr | 94 |

| Employee Benefits | 5.1.2 | 2 | Dr | 95 |

| Services | 5.1.3 | 2 | Dr | 96 |

| Rent, Depreciation, Amortization and Depletion | 5.1.4 | 2 | Dr | 97 |

| Expenses (Classified by Function) | 5.2 | 1 | Dr | 98 |

| Cost of Revenue | 5.2.1 | 2 | Dr | 99 |

| Selling, General and Administrative Expense | 5.2.2 | 2 | Dr | 100 |

| Other Non-operating Income and Expenses | 6 | 0 | Dr or (Cr) | 101 |

| Other Revenue and Expenses | 6.1 | 1 | Dr or (Cr) | 102 |

| Other Revenue | 6.1.1 | 2 | (Cr) | 103 |

| Other Expenses | 6.1.2 | 2 | Dr | 104 |

| Gains and Losses | 6.2 | 1 | Dr or (Cr) | 105 |

| Taxes Other Than Income and Payroll and Fees | 6.3 | 1 | Dr | 106 |

| Income Tax Expense or Benefit | 6.4 | 1 | Dr or (Cr) | 107 |

| Intercompany and related party accounts | 7 | 0 | Dr or (Cr) | 108 |

| Intercompany and related party assets | 7.1 | 1 | Dr | 109 |

| Intercompany balances eliminated in consolidation | 7.1.1 | 2 | Dr | 110 |

| Related party balances reported or disclosed | 7.1.2 | 2 | Dr | 111 |

| Intercompany investments | 7.1.3 | 2 | Dr | 112 |

| Intercompany and related party liabilities | 7.2 | 1 | (Cr) | 113 |

| Intercompany balances eliminated in consolidation | 7.2.1 | 2 | (Cr) | 114 |

| Related party balances reported or disclosed | 7.2.2 | 2 | (Cr) | 115 |

| Intercompany and related party income and expense | 7.3 | 1 | Dr or (Cr) | 116 |

| Intercompany and related party income | 7.3.1 | 2 | (Cr) | 117 |

| Intercompany and related party expenses | 7.3.2 | 2 | Dr | 118 |

| Income loss from equity method investments | 7.3.3 | 2 | Dr or (Cr) | 119 |

Updated: January 2026.

The 2026 XBRL version has been updated with cross-references to the 2026 FASB issued XBRL taxonomy.

The COA published on this page may be republished provided the following citation is provided: