A basic GAAP chart of accounts is presented below.

This chart of accounts is compatible with GAAP and comparable accounting standards.

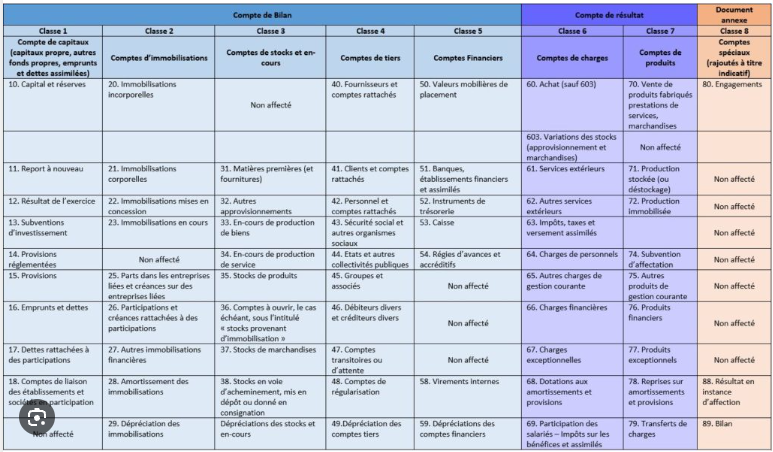

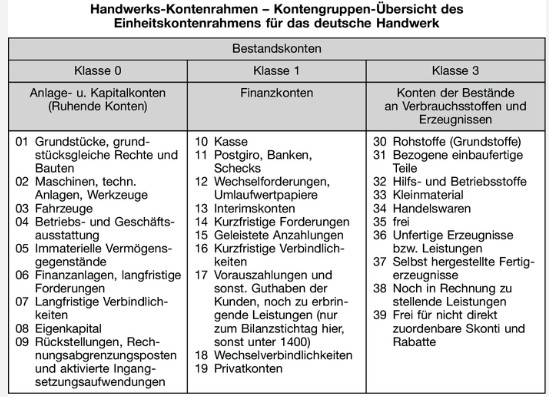

A number of EU member states, for example France and Germany, mandate a chart of accounts.

Similar rules may be found in China, Russia, OHADA member states and elsewhere.

Required by French law

Required by German law

In these jurisdictions, deviating from the prescribed COA may not be permissible or only in specific scenarios.

For example, French (link: anc.gouv.fr) accounting standard Art. 1222-70 (view pdf) states: "Les montants des ventes, des prestations de services, des produits afférents aux activités annexes sont enregistrés au crédit des comptes 701 « Ventes de produits finis », 702 « Ventes de produits intermédiaires », 703 « Ventes de produits résiduels », 704 « Travaux », 705 « Études », 706 « Prestations de services », 707 « Ventes de marchandises » et 708 « Produits des activités annexes ». Les rabais, remises et ristournes accordés hors facture ou qui ne sont pas rattachables à une vente déterminée sont portés au débit du compte 709 « Rabais, remises et ristournes accordés ». Version 1er janvier 2026 Page 180 sur 181 Même lorsqu'ils sont déduits sur la facture de vente, les escomptes de règlement sont comptabilisés au débit du compte 665 « Escomptes accordés »."

Deviating from the French COA by not using accounts 701 to 708 would be inconsistent with this legislation.

Some jurisdictions allow or require certain entities to apply IFRS alongside, or in place of, national GAAP in certain scenarios. In such jurisdictions, the COAs presented here could be used provided they do not conflict with other legislation.

For example, in the Czech Republic, the Accounting Act 563/1991 paragraph §19a (1) states:

"An [unconsolidated] entity that is a trading company and is an issuer of investment securities admitted to trading on a European regulated market shall apply international accounting standards regulated by European Union law (hereinafter referred to as "international accounting standards") for accounting and the preparation of financial statements" [paragraph § 23a requires IFRS at the consolidated entity level].

This implies, if the COA presented here is used for IFRS bookkeeping purposes and IFRS recognition guidance is applied correctly, it may (implicitly) be used in place of the chart of accounts mandated by the same law but only by a trading company (consolidated entity) that is an issuer of investment securities admitted to trading on a European regulated market.

Nevertheless, the Income Tax Act 586/1992 §23 (2) states:

"The tax base is determined a) from the net income (profit or loss), always without the influence of International Accounting Standards, for taxpayers required to maintain accounts. A taxpayer that prepares financial statements in accordance with International Accounting Standards regulated by European Community shall apply for the purposes of this Act to determine net income and to determine other data decisive for determining the tax base a special legal regulation [CZ GAAP]). When determining the tax base, entries in off-balance sheet account books are not taken into account, unless otherwise provided in this Act. ..."

Thus, since Czech accounting law assumes the mandated chart of accounts will be used for accounting purposes, if a different chart of accounts is used, it will need to yield the same result as if the mandated chart of accounts were used. While this is not impossible with careful mapping and associated adjustments, it is generally more practical to use the mandated national GAAP COA for Czech accounting and taxation purposes, and a separate IFRS compatible COA for IFRS recognition, measurement, reporting, and disclosure purposes.

This site strongly encourages users to consult qualified, national experts before using its COAs for external, particularly tax and/or statutory, reporting purposes.

In contrast, the standardized chart of accounts on this page should be used in a dual-reporting environment instead.

Due to its liquidity, numerous entities have a secondary listing on a US capital market. While the SEC does allow foreign private issuers to present IFRS financial reports to US investors, these have traditionally applied a discount to entities not publishing US GAAP financial reports. Consequently, a significant number of dual filers publish a US GAAP report alongside an IFRS or national GAAP report. Using a chart of accounts designed for dual reporting purposes make this approach more practical.

Professional grade GAAP charts of accounts are also available for download. See:

All files are downloadable in .xlsx format in . They may also be purchased individually on this page.

Import into some ERP systems may require a .csv format.

As the COAs utilize a comma (see implementation guidance page), instead of saving as CSV in Excel, the COA should be saved as tab-delimited text for best results.

Alternatively, install Python (with Pandas and Openpyxl libraries) and download this file Excel-to-CSV.zip.

Rename the COA to 'Excel-TSV-Input.xlsx' and run the script.

Note: conversion to CSV strips the formatting necessary for the scripts on this page to function as designed. Use the Depth column to rebuild the hierarchy, before running these scripts.

The COA files are downloadable in .xlsx format.

Import into some ERP systems may require a CSV format.

As the COAs already utilize the comma, instead of saving as CSV in Excel the COA should be saved as tab-delimited text for best results.

Alternatively, install Python (with Pandas and Openpyxl libraries) and download this file Excel-to-CSV.zip.

Rename the COA to 'Excel-TSV-Input.xlsx' and run the script.

Note: conversion to CSV strips the formatting necessary for the scripts on this page to function as designed. Use the Depth column to rebuild the hierarchy, before running these scripts.

| Account Title | Account # | Depth | Balance | 1 |

| Assets | 1 | 0 | Dr | 2 |

| Cash, Cash Equivalents and Investments | 1.1 | 1 | Dr | 3 |

| Cash and Cash Equivalents | 1.1.1 | 2 | Dr | 4 |

| Investments | 1.1.2 | 2 | Dr | 5 |

| Receivables and Contracts | 1.2 | 1 | Dr | 6 |

| Accounts, Notes and Loans Receivable | 1.2.1 | 2 | Dr | 7 |

| Contracts With Customers | 1.2.2 | 2 | Dr | 8 |

| Nontrade and Other Receivables | 1.2.3 | 2 | Dr | 9 |

| Inventory | 1.3 | 1 | Dr | 10 |

| Merchandise | 1.3.1 | 2 | Dr | 11 |

| Raw Material, Parts and Supplies | 1.3.2 | 2 | Dr | 12 |

| Work in Process | 1.3.3 | 2 | Dr | 13 |

| Finished Goods | 1.3.4 | 2 | Dr | 14 |

| Other Inventory | 1.3.5 | 2 | Dr | 15 |

| Accruals and Additional Assets | 1.4 | 1 | Dr | 16 |

| Prepaid Expense | 1.4.1 | 2 | Dr | 17 |

| Accrued Income | 1.4.2 | 2 | Dr | 18 |

| Additional Assets | 1.4.3 | 2 | Dr | 19 |

| Property, Plant and Equipment | 1.5 | 1 | Dr | 20 |

| Land and Land Improvements | 1.5.1 | 2 | Dr | 21 |

| Buildings, Structures and Improvements | 1.5.2 | 2 | Dr | 22 |

| Machinery and Equipment | 1.5.3 | 2 | Dr | 23 |

| Furniture and Fixtures | 1.5.4 | 2 | Dr | 24 |

| Right of Use Assets (Classified as PP&E) | 1.5.5 | 2 | Dr | 25 |

A right to use an asset is a contractual right. Thus, the right-to-use asset (ROU) is, strictly speaking, always intangible. Nevertheless, the FASB-defined XBRL taxonomy includes: PropertyPlantAndEquipmentAndFinanceLeaseRightOfUseAssetAfterAccumulatedDepreciationAndAmortizationAbstract.

This implies that the right to use, for example, a building would comprise PP&E.

Note: provided the right-of-use asset is recognised on the balance sheet, the guidance (ASC 842-20-45-1 to 3) is flexible about how it is presented. For example, a leased building may be presented within the “Buildings” line item rather than on a separate “right-of-use asset” line, as long as the notes explain that the amount relates to a leased (right-of-use) building rather than an owned building. From an internal accounting perspective, the building could thus be posted either to the Buildings account with a metadata flag indicating that it is an ROU or to the ROU account with metadata describing the underlying asset as a building.

| Additional Property, Plant and Equipment | 1.5.6 | 2 | Dr | 26 |

| Construction in Progress | 1.5.7 | 2 | Dr | 27 |

| Intangible Assets Excluding Goodwill | 1.6 | 1 | Dr | 28 |

| Intellectual Property | 1.6.1 | 2 | Dr | 29 |

| Computer Software | 1.6.2 | 2 | Dr | 30 |

| Trade and Distribution Assets | 1.6.3 | 2 | Dr | 31 |

| Contracts and Rights | 1.6.4 | 2 | Dr | 32 |

| Right of Use Assets | 1.6.5 | 2 | Dr | 33 |

A right to use an asset is a contractual right. Thus, the right-to-use asset (ROU) is, strictly speaking, always intangible. Nevertheless, the FASB-defined XBRL taxonomy includes : PropertyPlantAndEquipmentAndFinanceLeaseRightOfUseAssetAfterAccumulatedDepreciationAndAmortizationAbstract.

This implies the right to use, for example, a building should be classified an ROU within PP&E (above) even though the right is clearly intangible.

With intangible assets, such issues do not arise.

However, while both are clearly intangible, a, for example, leased patent differs from an owned patent. Nevertheless, recognizing both owned and leased patents on the same "Patents" account would not be incorrect, and would actually be preferable, provided additional metadata (facilitating the required footnoted discloses) is associated with the leased patents.

Alternatively, while not particularly elegant, separate "Patent" and "Right-to-use Patent" accounts could be used. While it would lead to fragmented and counterintuitive accounting, it would not be inconsistent with the the guidance.

ASC 842-20-45-1 states (emphasis added): A lessee shall either present in the statement of financial position or disclose in the notes all of the following: a. Finance lease right-of-use assets and operating lease right-of-use assets separately from each other and from other assets ...

ASC 842-20-45-2 clarifies this guidance by stating: If a lessee does not present finance lease and operating lease right-of-use assets and lease liabilities separately in the statement of financial position, the lessee shall disclose which line items in the statement of financial position include those right-of-use assets and lease liabilities.

In practice, the preferred approach would be to recognize, for example, both owned and leased patents as "Patents" and simply provide additional discourse of the values of the leased versus owned patents.

It would not, however, be incorrect to recognize owned patents as "Patents" and leased patents as "Rights to Use Patents" in which case, assuming the values are clearly distinguished on the balance sheet, they would not need to be reiterated in the footnotes.

| Crypto Assets | 1.6.6 | 2 | Dr | 34 |

While crypto assets have more in common with financial assets than intangible assets, ASC 350-60-15-1.a defines: a. Meet the definition of intangible assets as defined in the Codification ... d. Are secured through cryptography... The 2026 FASB-approved XBRL taxonomy (link) likewise places CryptoAssetFairValue on the balance sheet as a separate line item directly below intangible assets and above right-of-use assets.

| Additional Intangible Assets | 1.6.7 | 2 | Dr | 35 |

| Acquisition in Progress | 1.6.8 | 2 | Dr | 36 |

| Goodwill | 1.7 | 1 | Dr | 37 |

| Liabilities | 2 | 0 | (Cr) | 38 |

| Payables | 2.1 | 1 | (Cr) | 39 |

| Trade Payables | 2.1.1 | 2 | (Cr) | 40 |

| Interest Payable | 2.1.2 | 2 | (Cr) | 41 |

| Dividends Payable | 2.1.3 | 2 | (Cr) | 42 |

| Other Payables | 2.1.4 | 2 | (Cr) | 43 |

| Accruals, Deferrals and Additional Liabilities | 2.2 | 1 | (Cr) | 44 |

| Accrued Expenses | 2.2.1 | 2 | (Cr) | 45 |

| Deferred Revenue and Refund Liabilities | 2.2.2 | 2 | (Cr) | 46 |

| Taxes Other Than Payroll | 2.2.3 | 2 | (Cr) | 47 |

| Additional Liabilities | 2.2.4 | 2 | (Cr) | 48 |

| Financial Liabilities | 2.3 | 1 | (Cr) | 49 |

| Notes Payable | 2.3.1 | 2 | (Cr) | 50 |

| Loans Payable | 2.3.2 | 2 | (Cr) | 51 |

| Bonds | 2.3.3 | 2 | (Cr) | 52 |

| Other Debts and Liabilities | 2.3.4 | 2 | (Cr) | 53 |

| Lease Obligations | 2.3.5 | 2 | (Cr) | 54 |

| Derivative Liabilities | 2.3.6 | 2 | (Cr) | 55 |

| Commitments and Contingencies | 2.4 | 1 | (Cr) | 56 |

| Customer Related Contingencies | 2.4.1 | 2 | (Cr) | 57 |

| Litigation and Regulatory | 2.4.2 | 2 | (Cr) | 58 |

| Additional Obligations | 2.4.3 | 2 | (Cr) | 59 |

| Commitments | 2.4.4 | 2 | (Cr) | 60 |

| Equity | 3 | 0 | (Cr) | 61 |

| Equity, Attributable to Parent | 3.1 | 1 | (Cr) | 62 |

| Stockholders Equity at Par | 3.1.1 | 2 | (Cr) | 63 |

| Additional Paid-in Capital | 3.1.2 | 2 | (Cr) | 64 |

| Retained Earnings (Accumulated Deficit) | 3.2 | 1 | (Cr) | 65 |

| Appropriated | 3.2.1 | 2 | (Cr) | 66 |

| Unappropriated | 3.2.2 | 2 | (Cr) | 67 |

| Deficit | 3.2.3 | 2 | Dr | 68 |

| In Suspense | 3.2.4 | 2 | Zero | 69 |

| Accumulated Other Comprehensive Income | 3.3 | 1 | Dr or (Cr) | 70 |

| Other Equity Items | 3.4 | 1 | Dr or (Cr) | 71 |

| ESOP Related Items | 3.4.1 | 2 | (Cr) | 72 |

| Stock Receivables | 3.4.2 | 2 | Dr | 73 |

| Treasury Stock | 3.4.3 | 2 | Dr | 74 |

| Additional Equity Items | 3.4.4 | 2 | (Cr) | 75 |

| Owners Equity | 3.5 | 1 | (Cr) | 76 |

| Partner's Capital | 3.5.1 | 2 | (Cr) | 77 |

| Member's Equity | 3.5.2 | 2 | (Cr) | 78 |

| Non-share Equity | 3.5.3 | 2 | (Cr) | 79 |

| Non-controlling Minority Interest | 3.6 | 1 | (Cr) | 80 |

| Revenue | 4 | 0 | (Cr) | 81 |

| Recognized Point of Time | 4.1 | 1 | (Cr) | 82 |

| Goods | 4.1.1 | 2 | (Cr) | 83 |

| Services | 4.1.2 | 2 | (Cr) | 84 |

| Recognized Over Time | 4.2 | 1 | (Cr) | 85 |

| Products and Projects | 4.2.1 | 2 | (Cr) | 86 |

| Services | 4.2.2 | 2 | (Cr) | 87 |

| Adjustments | 4.3 | 1 | Dr | 88 |

| Variable Consideration | 4.3.1 | 2 | Dr | 89 |

| Consideration Paid Payable to Customers | 4.3.2 | 2 | Dr | 90 |

| Other Adjustments | 4.3.3 | 2 | Dr | 91 |

| Expenses | 5 | 0 | Dr | 92 |

| Expenses (Classified by Nature) | 5.1 | 1 | Dr | 93 |

| Material and Merchandise | 5.1.1 | 2 | Dr | 94 |

| Employee Benefits | 5.1.2 | 2 | Dr | 95 |

| Services | 5.1.3 | 2 | Dr | 96 |

| Rent, Depreciation, Amortization and Depletion | 5.1.4 | 2 | Dr | 97 |

| Expenses (classified by function) ⚠ | 5.2 | 1 | Dr | 98 |

For accounting purposes, expenses should be recognized by nature and their function treated as a reporting attribute.

In practice, however, expenses may be both recognized and reported by function even though this leads to duplicate accounts such as Employee compensation: Production, Employee compensation: Sales, Employee compensation: Administration as well as Depreciation: Production equipment, Depreciation: Sales equipment, Depreciation: Office equipment.

While not disallowed, this approach is not recommended particularly because (from December 16, 2026) ASC 220-40-50-6 requires nature of expense items (a. purchases of inventory, b. employee compensation, c. depreciation, d. intangible asset amortization e. depletion and addition items associated with oil or gas-producing activities) to be disclosed in a tabular format in the notes to financial statements.

Important: nature / function of expense classification may not both be used as this would lead to expense double counting.

| Cost of sales | 5.2.1 | 2 | Dr | 99 |

| Selling, general and administrative | 5.2.2 | 2 | Dr | 100 |

| Other Revenue, Expenses, Gains and Losses | 6 | 0 | Dr or (Cr) | 101 |

Traditionally, charts of accounts have been divided into five basic categories: 1. assets 2. liabilities, 3. equity, 4. revenue and 5. expense. Technically, as revenue less expense is accumulated in retained earnings, which is a subclassification of equity, 3 categories would be sufficient.

Nevertheless, revenue and expense are critically important both for accounting and reporting purposes, so the tradition of treating them as basic classifications is valid.

However, not all revenue and expense have the same character nor significance.

For example revenue from the sale of goods and services, cost of sales, selling expenses, administrative expenses, general expenses are key to capturing and reporting an entity's operations and performance. Perhaps more importantly, for financial statement users, they have significant predictive value. In contrast, interest paid or interest received (except for financial institutions) is comparatively less significant and, as interest is often dictated by market conditions, has little, if any, predictive value for users evaluating operating results.

Further down the spectrum, gains and losses, generally the result of changes in fair value over which an entity has no control, while needing to be accounted for, are usually uncorrelated with an entity's operations so of little use when evaluating an entity’s performance and have little, if any, predictive value.

Thus, instead of the traditional 5 basic categories, this chart of accounts includes 6. This section thus comprises non-operating revenue and expense as well as gains and losses.

Note: this structure is fully consistent with chapter 4 of US GAAP’s conceptual framework, particularly paragraphs E84 and E85.

| Other Revenue and Expenses | 6.1 | 1 | Dr or (Cr) | 102 |

| Other Revenue | 6.1.1 | 2 | (Cr) | 103 |

| Other Expenses | 6.1.2 | 2 | Dr | 104 |

| Gains and Losses | 6.2 | 1 | Dr or (Cr) | 105 |

| Taxes Other Than Income and Payroll and Fees | 6.3 | 1 | Dr | 106 |

| Income Tax Expense or Benefit | 6.4 | 1 | Dr or (Cr) | 107 |

| Intercompany and related party accounts | 7 | 0 | Dr or (Cr) | 108 |

| Intercompany and related party assets | 7.1 | 1 | Dr | 109 |

| Intercompany balances eliminated in consolidation | 7.1.1 | 2 | Dr | 110 |

| Related party balances reported or disclosed | 7.1.2 | 2 | Dr | 111 |

| Intercompany investments | 7.1.3 | 2 | Dr | 112 |

| Intercompany and related party liabilities | 7.2 | 1 | (Cr) | 113 |

| Intercompany balances eliminated in consolidation | 7.2.1 | 2 | (Cr) | 114 |

| Related party balances reported or disclosed | 7.2.2 | 2 | (Cr) | 115 |

| Intercompany and related party income and expense | 7.3 | 1 | Dr or (Cr) | 116 |

| Intercompany and related party income | 7.3.1 | 2 | (Cr) | 117 |

| Intercompany and related party expenses | 7.3.2 | 2 | Dr | 118 |

| Income loss from equity method investments | 7.3.3 | 2 | Dr or (Cr) | 119 |