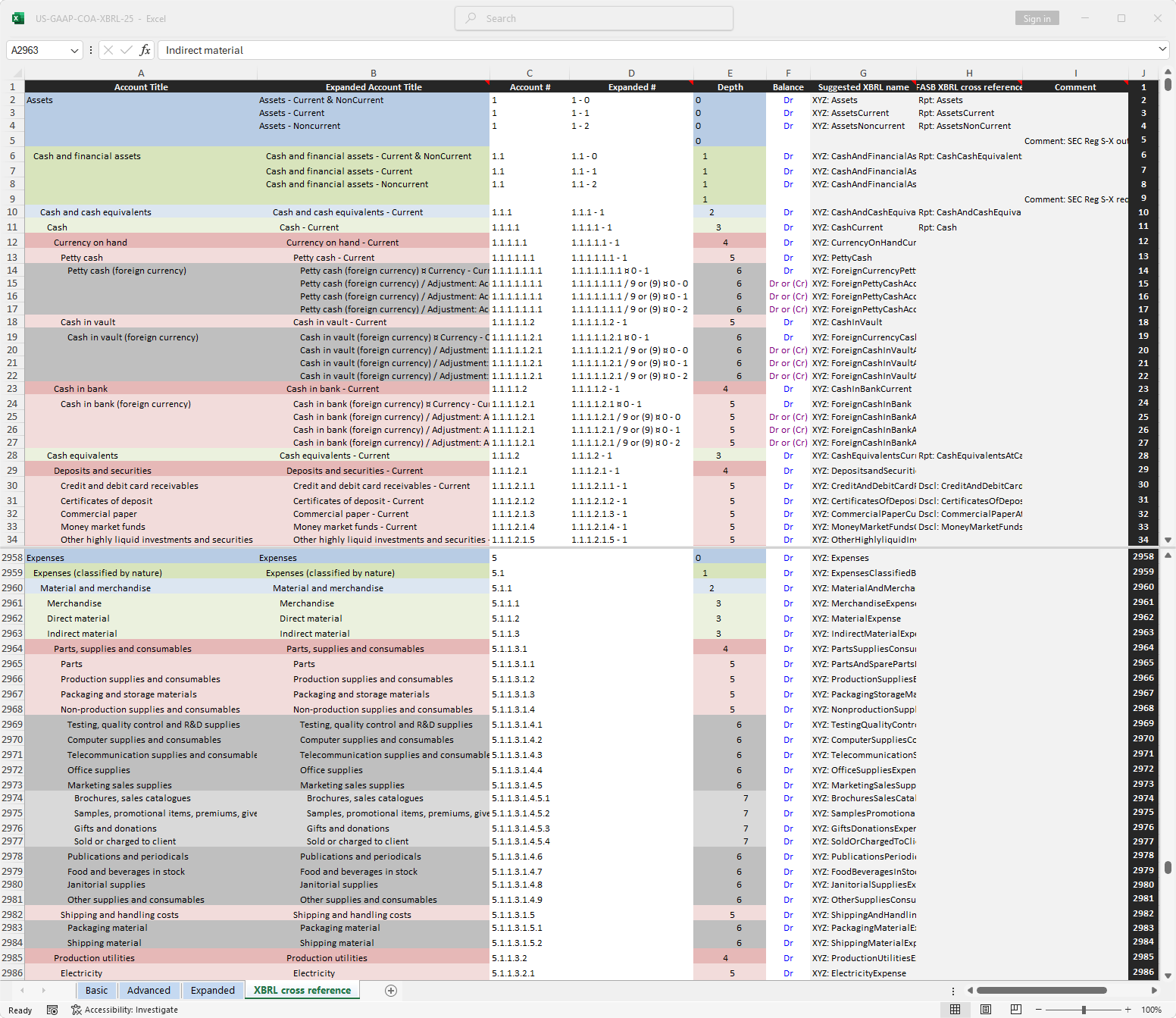

Download the XBRL cross referenced GAAP COA in .xlsx professional view.

Professional view costs €89.90 for one year.

Professional view does not renew automatically.

Get professional view or log in.

Additional guidance on how to implement a COA is provided on this page.

The downloadable COA provides a perfectly adequate, ready‑to‑use fit. While perfectly workable, some companies prefer the tailored feel of a bespoke solution. This customization may be handled in‑house. However, the considerable effort and cost can be avoided by having a fully configured COA made to measure.

Mapping these COAs to financial statements that mirror their layout can likewise be easily automated as illustrated by the simple scripts posted to this page.

Prices for tailored COAs mapped to custom financial statements start at €500. Please contact us for an estimate.