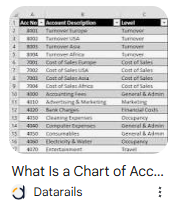

Basic charts of accounts address the fundamental recognition requirements of the guidance.

IFRS is the most widely accepted standard. As such, it provides a solid basis for a chart of accounts. When reflected in the accounts, this guidance can serve as the basis for a COA applicable in any compatible jurisdiction.

Additional versions of this basic chart of accounts are available for download in .

All COA files on this site are available for download in .xlsx format.

While Excel is a lingua franca, some ERP systems require a CSV or TSV format instead.

To perform the conversion, make certain you have Python with Pandas and Openpyxl libraries installed. Next, download Excel-to-CSV.zip. Place both the COA and the script into the same folder. Rename the COA exactly Excel-TSV-Input.xlsx and run the script.

To convert back to Excel, copy Excel-TSV-Output.csv to Excel and use the Text to Columns function. Leave the delimiter set to the default Tab. Please be aware, the conversion process strips formatting, so the Depth column is critical for rebuilding COA's hierarchy and make the scripts on this page function correctly.

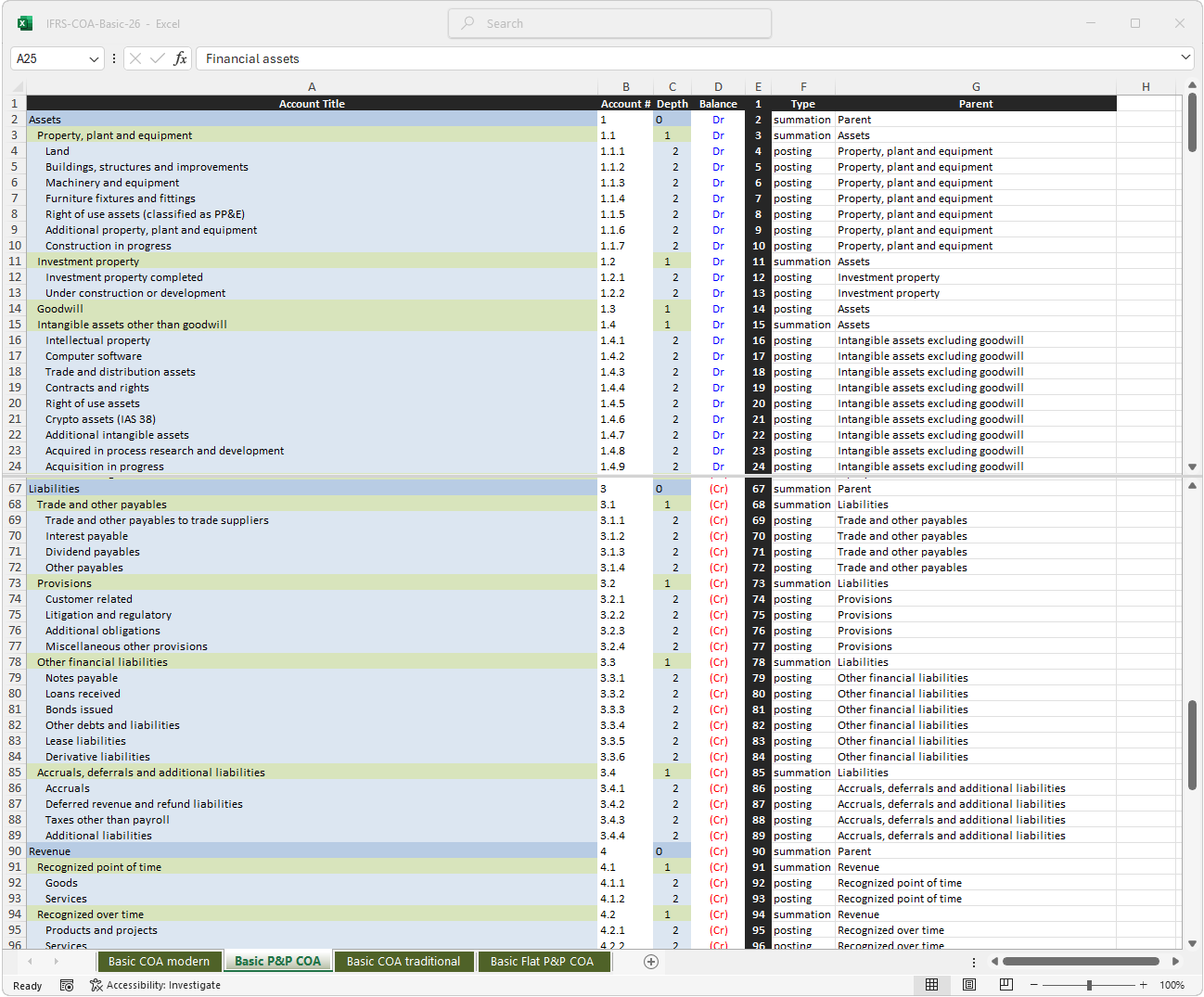

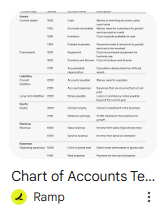

The above plug-and-play version includes explicit posting / summation data and is suitable for import into a basic ERP system.

Using a recursive aggregation engine as outlined on the implementation guidance page, the account structure would adapt dynamically to the data. As such, it would be unnecessary to explicitly denote posting / summation accounts.

Explicitly defined account numbers would likewise be optional.

However, this does assume a dimensional ERP installation sufficiently flexible to facilitate this approach.

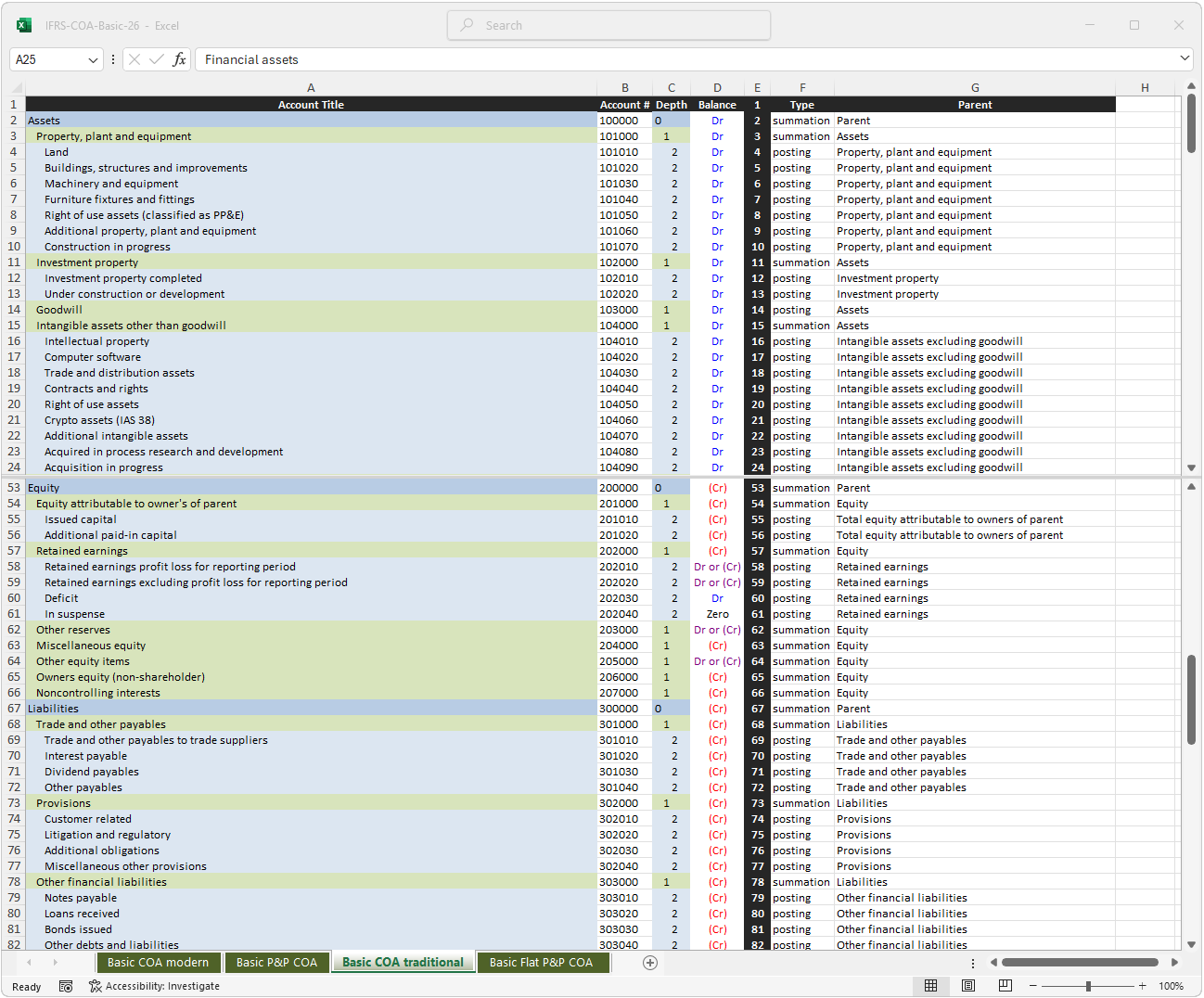

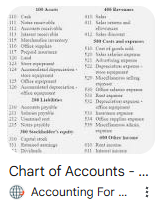

The above block numbered version also employs a traditional numbering scheme.

Many COA designers stick with block numbering for the sake of tradition (click to enlarge):

While flat block numbering makes the COA cumbersome, the expanded block included in the downloadable version makes the COA somewhat less cumbersome.

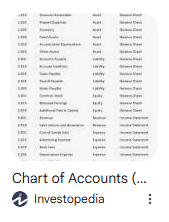

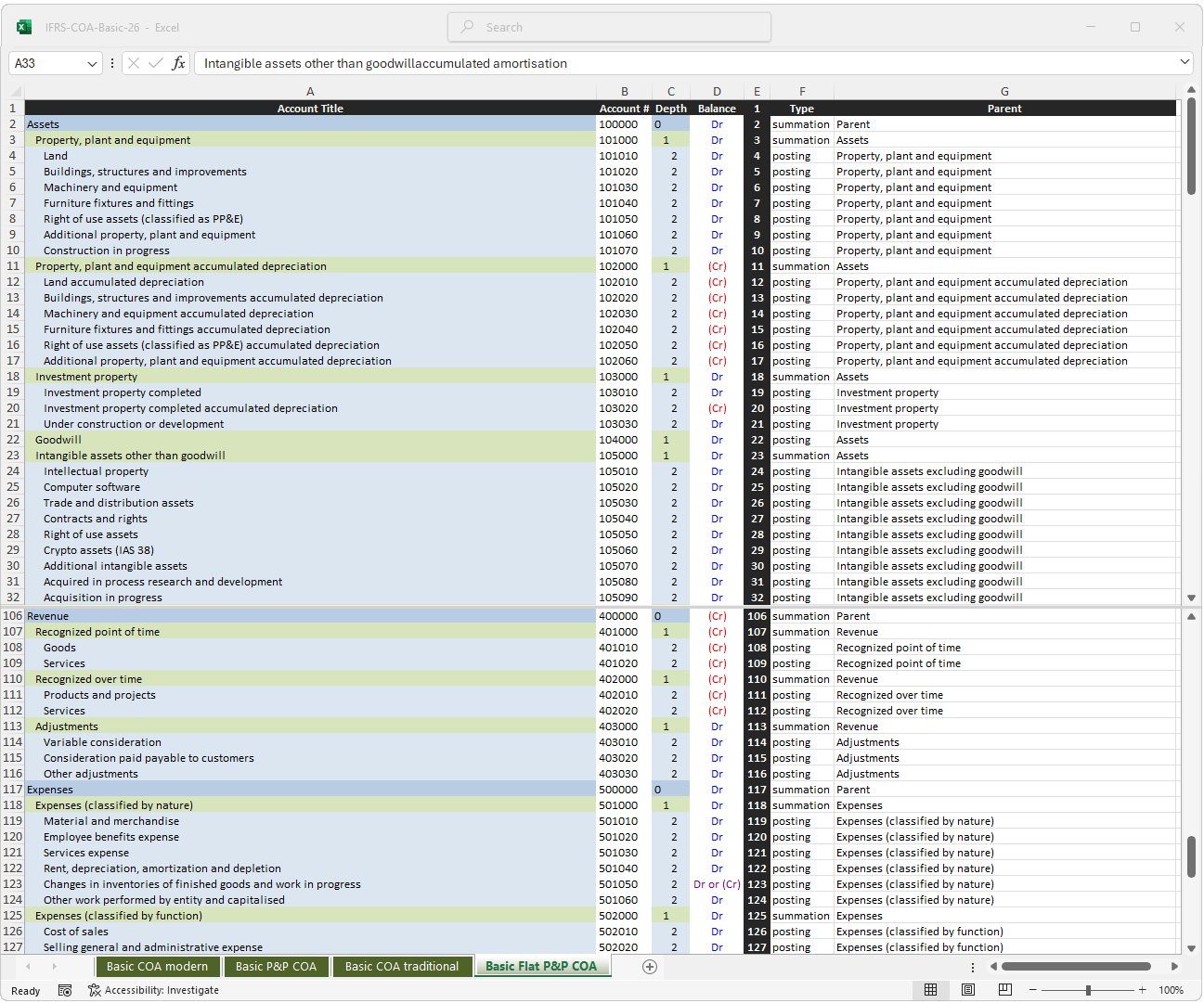

The above flat, block numbered version takes an additional step in the direction of tradition.

The flat, block numbering system, that treats adjustments such as accumulated depreciation as separate accounts, continues to be taught some.

Requiring the least investment in technology, it can be used with the most budget friendly ERP systems. It would also be suitable for the most budget friendly option of all: keeping the books in Excel.