Downloads of this chart in .xlsx are available in professional view.

Professional view costs €89.90 for one year.

Professional view does not renew automatically.

Get professional view or log in.

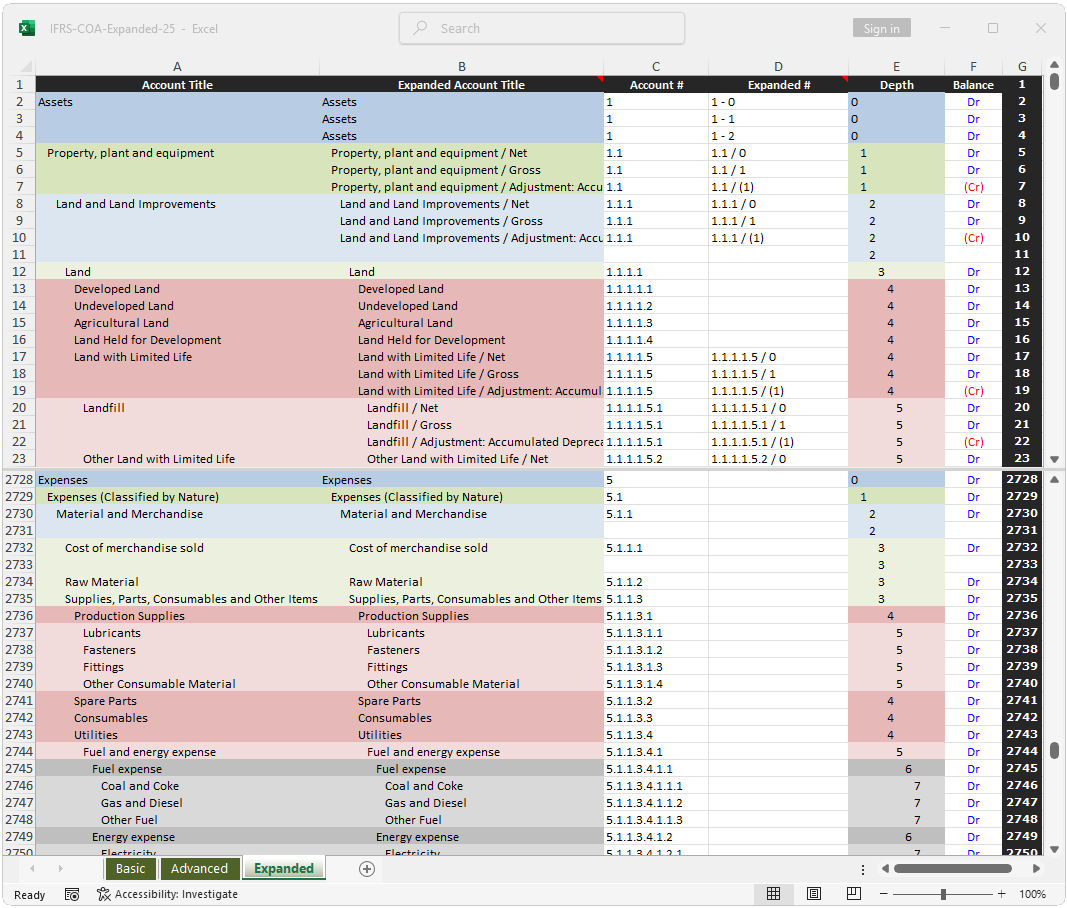

This chart of accounts includes extended IFRS compatible classifications.

The IASB does not publish an "IFRS chart of accounts".

Companies may use any chart of accounts, provided it is consistent with published recognition guidance (link: eifrs.ifrs.org).

This chart has been designed to be consistent with this guidance.

While users may delete unnecessary / add additional sub-accounts, they are advised to keep its general structure intact.

eXtensible Business Reporting Language is a reporting language.

"In a nutshell, XBRL provides a language in which reporting terms can be authoritatively defined. Those terms can then be used to uniquely represent the contents of financial statements or other kinds of compliance, performance and business reports. XBRL lets reporting information move between organisations rapidly, accurately and digitally" (link: xbrl.org).

It is not a chart of accounts.

The chart of accounts presented here includes XBRL cross references to ease the drafting of XBRL taged financial reports.

Some items necessary for accounting do not have a defined (link: ifrs.org). XBRL counterpart.

These items are labled "_Extension" and presented in a different color to avoid confusion.

IFRS XBRL is also viewable online (link: corefiling.com).

This chart does makes a current/non-current distinction.

The current / non-current status of an item is a reporting rather than recognition issue, incorporating a current / non-current distinction into the account structure not only adds unnecessary complexity, but can lead to unnecessary item reclassifications.

IAS 1.60 An entity shall present current and non-current assets, and current and non-current liabilities, as separate classifications in its statement of financial position in accordance with paragraphs 66–76 except when a presentation based on liquidity provides information that is reliable and more relevant. When that exception applies, an entity shall present all assets and liabilities in order of liquidity.

Nevertheless, as some companies prefer a chart of accounts that makes this distinction, a current / non-current chart of accounts is available to subscribers.

This chart includes expenses classified by both nature and function.

IFRS requires nature of expense disclosure, and permits both function and nature of expense reporting.

IAS 1.104 An entity classifying expenses by function shall disclose additional information on the nature of expenses, including depreciation and amortisation expense and employee benefits expense.

IAS 1.99 An entity shall present an analysis of expenses recognised in profit or loss using a classification based on either their nature or their function within the entity, whichever provides information that is reliable and more relevant.

From an accounting perspective, a nature based account structure yields superior operational results.

For a more detailed example see: Nature of expense, function of expense.

For example, if accounts were organized by function, the result will resemble:

| --- | --- |

| Expenses Classified By Function | 5.2 |

| Cost Of Sales | 5.2.1 |

| Emloyee benefits | 5.2.1.1 |

| Wages | 5.2.1.1.1 |

| Salaries | 5.2.1.1.2 |

| --- | --- |

| Selling, General And Administrative | 5.2.2 |

| Emloyee benefits | 5.2.2.1 |

| Wages | 5.2.2.1.1 |

| Salaries | 5.2.2.1.2 |

| Commissions | 5.2.2.1.3 |

| --- | --- |

When accounts are initially organized by nature, the result can resemble:

| Account | Department | ||

| --- | --- | --- | |

| Expenses Classified By Nature | 5.1 | ||

| Employee Benefits | 5.1.3 | ||

| Production department | 5.1.3 | - | 5.2.1 |

| Sales department | 5.1.3 | - | 5.2.2.1 |

| Administrative department | 5.1.3 | - | 5.2.2.2 |

| --- | --- |

Also note, while it would be possible to add a digit for country of domicile, subsidiary, segment, reporting unit etc., in practice it is more practical for each such entity to maintain separate accounts, which are then consolidated:

| Country | Account | Department | |||

| --- | --- | ||||

| Employee Benefits - UK | 1 | - | 5.1.3 | ||

| Production department - UK | 1 | - | 5.1.3 | - | 5.2.1 |

| Sales department - UK | 1 | - | 5.1.3 | - | 5.2.2.1 |

| Administrative department - UK | 1 | - | 5.1.3 | - | 5.2.2.2 |

| --- | --- | ||||

| Employee Benefits - France | 2 | - | 5.1.3 | ||

| Production department - France | 2 | - | 5.1.3 | - | 5.2.1 |

| Sales department - France | 2 | - | 5.1.3 | - | 5.2.2.1 |

| Administrative department - France | 2 | - | 5.1.3 | - | 5.2.2.2 |

| --- | --- |

This chart includes adjustments such as accumulated depreciation and amortization.

This chart is an intermediate step between a basic chart and the advanced chart, in that using the advanced chart is recommended in practice.

Update: April, 2025.

Subscriber.xlsx