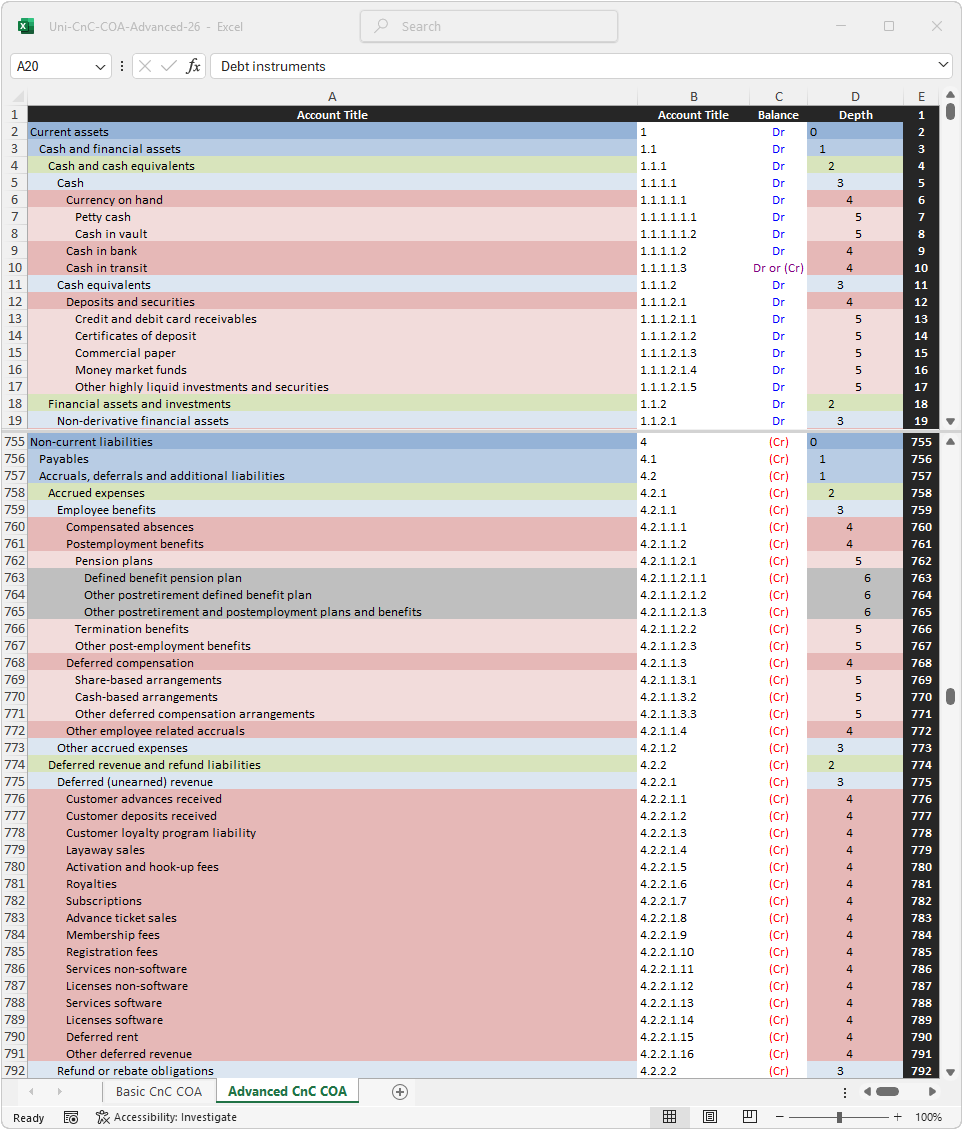

This COA reflects IFRS | US GAAP guidance in a current non-current format.

As discussed in more detail on the implementation page, a current/non-current format COA is impractical.

Nevertheless, as US GAAP requires and IFRS allows a current/non-current format balances sheet, aligning the COA to the fanatical report is relatively common in practice.

To reflect this practice, this page includes a current/non-current COA even though it does not recommend its use.

Note: as neither IFRS nor US GAAP provide any guidance on the structure of a COA, an order of liquidity structure (used on all the above COAs) may be used for both IFRES and US GAAP purposes without violating any guidance.